Preview:

A variety of approaches have been developed to evaluate pharmaceutical assets, but two similar yet distinct methods are most commonly used. Venture capitalists and large investment firms typically employ net present value (NPV) calculations while pharmaceutical companies more commonly use risk-adjusted net present value calculations (rNPV). This paper summarizes the limitations and benefits of each method and considers the current discount rates commonly applied by both investors and pharmaceutical companies.

About the authors

Jonathan Stasior interned at Alacrita during the summer of 2018 and is an Economics major at Williams College.

Brian Machinist is a Partner at Alacrita specializing in strategic planning, corporate development and marketing in the pharmaceutical, biotechnology and medical device industries.

Michael Esposito, a Partner at Alacrita, has for the last 30 years been involved in a variety of functional and corporate planning assignments for pharmaceutical, biotechnology, medical equipment/supply/ device companies and diagnostic companies around the world.

Alacrita's pharma valuation expertise

Our expertise in performing business and asset valuations covers a wide range of technology types, including small molecules, biologics and gene therapies across a variety of clinical indications.

Paper Download

Paper Text:

Accurately assessing the present value of pharmaceutical products during the various stages of research and development poses a challenge for drug developers and investors alike because of the low probability of a new drug successfully completing clinical trials and becoming approved. After discovery, an investigational new drug (IND) has an average probability of technical and regulatory success (PTRS) of 9.6%, but some therapeutic areas experience average success rates as low as 5.1% (1). The long period of performing clinical trials after discovery and before launch, which often takes more than ten years, further complicates determining the present value of an investigational new drug because cash flows occurring further in the future are subject to increased uncertainty and receive a significant discounting to account for the time value of money. A variety of approaches have been developed to evaluate in-process research and development (IPR&D) assets, but two similar yet distinct methods are commonly utilized. Venture capitalists and large investment firms typically employ net present value (NPV) calculations while pharmaceutical companies more commonly use risk-adjusted net present value calculations (rNPV) (2). This paper briefly summarizes the limitations and benefits of each method and considers the current discount rates commonly applied by both investors and pharmaceutical companies.

Both NPV and rNPV use a common discounted cash flow (DCF) approach, incorporating net cash flows, the discount rate and the number of years in development/on the market. The NPV method, however, employs an increased discount rate to account for the time value of money, commercial risk and the risk of failure during research and development. In comparison, the rNPV method uses a relatively smaller discount rate to account for the time value of money and commercial risk but also multiplies each cash flow at each stage of development by the probability of reaching that stage to account for the risk of research and development failure (3). Despite the differences in approaches, both methods can result in similar valuations at a given point in time if the discount rate used in the NPV calculation accurately reflects the overall probability of technical and regulatory success used in the rNPV calculation. The NPV method, however, fails to reflect the decreasing risk over time as the investigational new drug advances through the development process because a given discount rate can only represent the overall risk associated with an individual stage of development. The addition of probabilities of success at each stage of development included in the rNPV calculation gives it the added benefit of more accurately reflecting changes in risk and present value over time.

NPV

The standard NPV calculation requires knowledge of the expected revenues (cash inflows) and costs (cash outflows) for each year along with a general understanding of the current probability of technical and regulatory success. The cash flows for each year are simply discounted and then summed to obtain the NPV. Calculating the NPV of an asset requires both an accurate estimate of cash flows as well as selecting a discount rate that properly reflects the overall risk of the asset.

Investors naturally require a higher rate of return for riskier investments because of the increased likelihood that their returns will never materialize. The discount rate used, therefore, needs to correspond to the expected rate of return and the perceived risk of the investment.

In theory, the discount rate for calculating the net present value of a firm and its assets simply equals that firm’s weighted average cost of capital (WACC) or the rate of return needed to repay investors/debt holders. The weighted average cost of capital includes the combined cost of equity and the cost of debt, but because pharmaceutical R&D projects typically receive financing almost entirely through equity, the cost of equity component tends to dominate the weighted average cost of capital and the corresponding discount rate. Calculating the cost of equity requires utilizing the capital asset pricing model (CAPM), which defines the relationship between the risk and expected return of an investment. It states that the expected rate of return equals the risk-free rate plus the product of the risk premium and the beta coefficient, which represents the risk of that individual investment. Beta is calculated by dividing the covariance between the return of the asset and the return on the market by the variance in returns on the market (4).

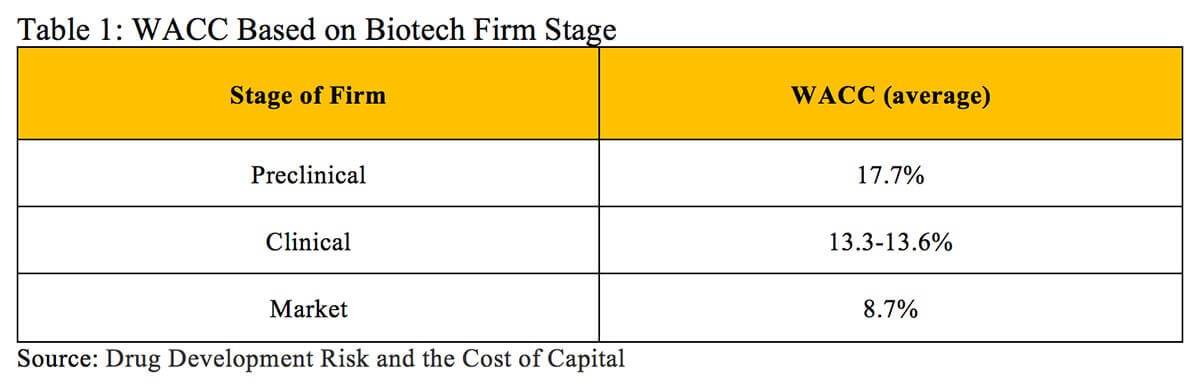

A 2012 analysis of publicly traded biotech firms in different stages calculated an average WACC of 17.7% for preclinical entities, 13.3-13.6% for clinical stage companies and 8.7% for market-stage firms (displayed in Table 1) (5).

This weighted average cost of capital approach works well for determining the beta of an asset that is publicly traded or where similar publicly traded assets/companies can be found. However, this approach can face several challenges. The first arises when a company is privately held and owns assets that cannot be easily compared to other assets with known betas. The second challenge occurs when companies develop a portfolio of multiple products with different betas. The discount rate found using the weighted average cost of capital reflects the aggregate risk of the company. While these discount rates can prove useful for calculating the NPV of the company’s entire portfolio, they can dramatically underestimate the appropriate discount rate that reflects risk associated with each individual product in development. This becomes especially true for products across various stages of development.

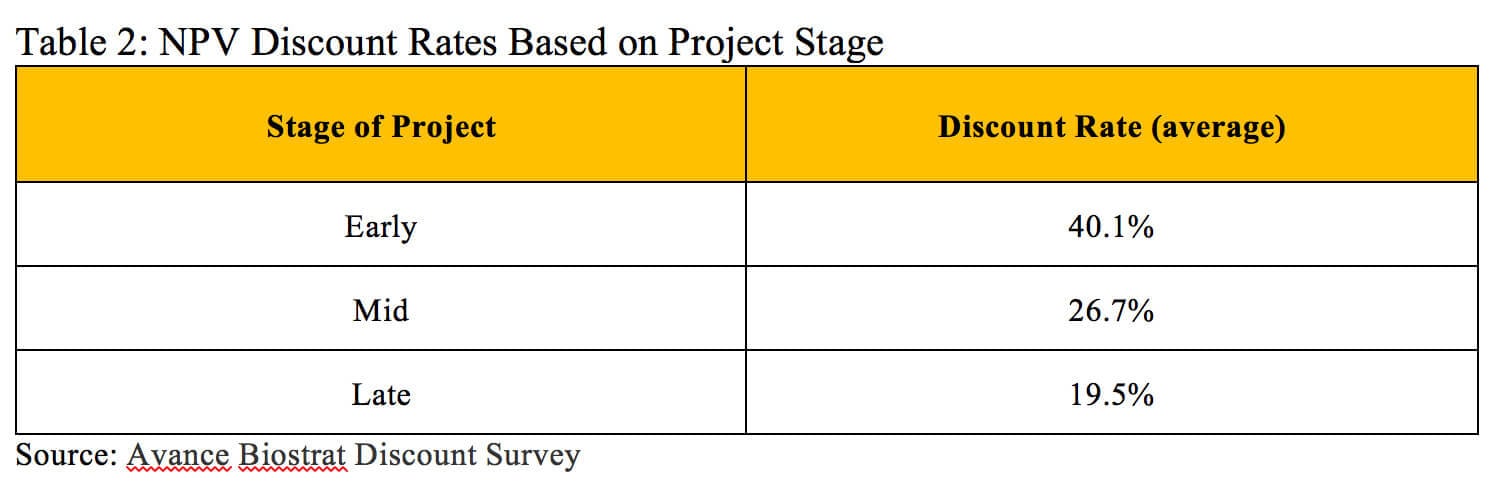

The alternative approach relies on general guidelines and industry benchmarks to estimate an appropriate discount rate. For early stage assets, the discount rate for a single pharmaceutical product can reach as high as 50% to reflect the low probability that the drug reaches the market. Discount rates closer to 20% are more appropriate when assessing the value of a drug in the later phases of clinical trials (6). A survey of 242 biotech professionals with valuation experience and using the NPV approach found an average discount rate of 40.1% for early-stage projects, 26.7% for mid-stage projects and 19.5% for late-stage projects (displayed in Table 2) (7).

rNPV

Determining the risk-adjusted net present value (rNPV), like NPV, also involves forecasting the revenues (cash inflows), costs (cash outflows) and their respective timing but additionally requires the relevant success rate(s) for each stage of development. Fortunately, a wealth of data exists about the historical probabilities of success for pharmaceutical R&D projects across a range of therapeutic areas, providing industry standards for calculating the expected cost and probability of success at each stage (8). To account for risk, the expected net cash flow for a given time period is multiplied by the probability of it occurring. If an investigational new drug has successfully advanced through the preclinical stages and is about to start Phase 1 clinical trials, the cost of Phase 1 would be weighted by 100%. This is because the cash outflow associated with Phase 1 represents a sunk cost; that cash outflow occurs regardless of whether or not Phase 1 constitutes a success once complete. The cash outflow associated with the cost of Phase 2 is weighted to reflect the success rate of Phase 1 because Phase 2 can only occur if the Phase 1 trial is successful. Similarly, the cash outflow of Phase 3 is weighted by the cumulative probability of reaching it, which equals the success rate of Phase 1 multiplied by the success rate of Phase 2, etc. The net cash flows of the product for each year after receiving FDA approval and typically until the patent runs out are risk-adjusted by the current overall probability of technical and regulatory success at that point in time based on its stage of development. Once the net cash flow of each time period has been correctly risk-adjusted, these cash flows are then discounted using an appropriate discount rate and the discounted cash flow approach.

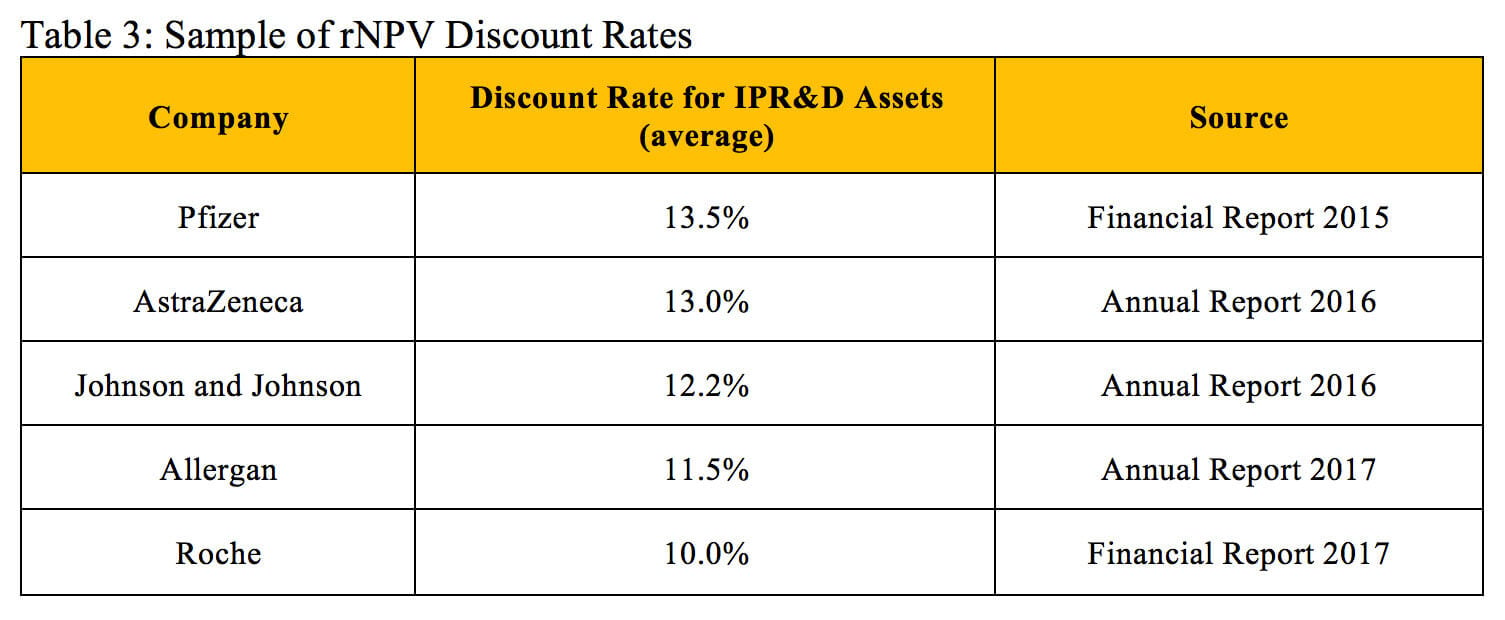

When performing rNPV evaluations for in-process research and development assets, pharmaceutical companies use different discount rates depending on their current cost of capital. These rates can vary but typically are in the range of 10 to 13%. A survey of large biotech companies found a median discount rate of 10% for evaluating internal R&D projects and external transaction opportunities (5). Table 3 displays the discount rates reported by five large pharmaceutical companies for evaluated in-process research and development assets.

While the discount rates used in rNPV calculations are fairly similar, the overall probabilities of technical and regulatory success often vary significantly. Selecting an appropriate probability of success depends on the investigational drug’s therapeutic area and stage of development (1).

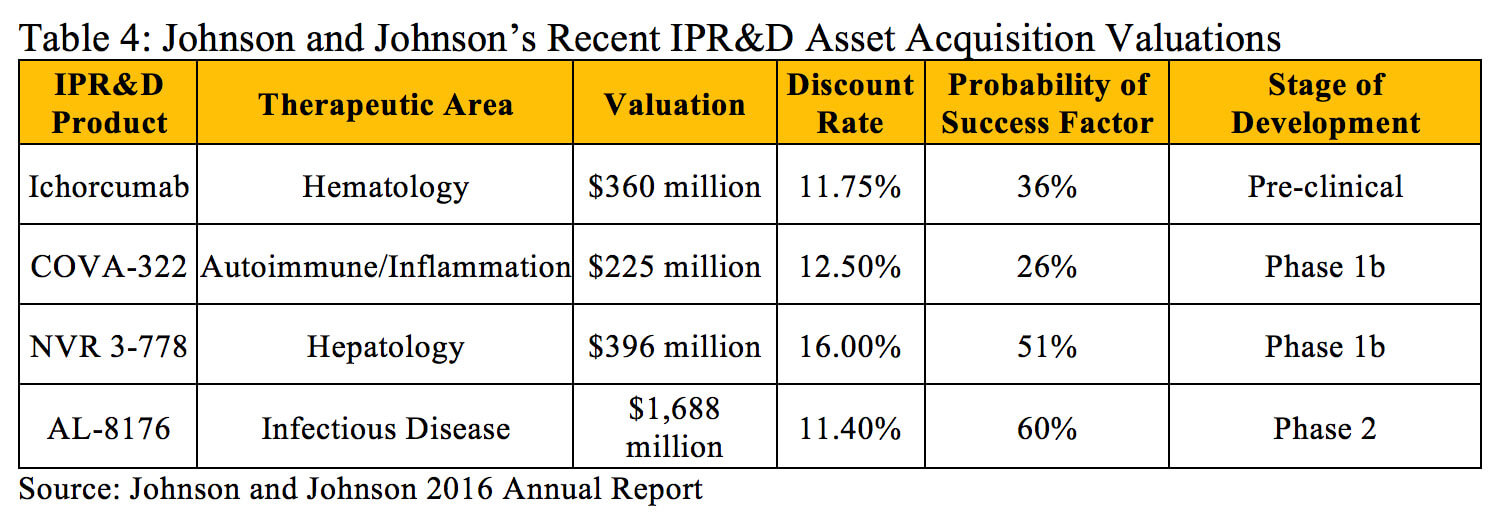

Within the literature, there are significant references that can be utilized to estimate the risk for various products in development based on the stage of development and therapeutic area. However, in some instances it is necessary to adjust these industry averages to reflect all current knowledge about a particular project. For example, Johnson and Johnson purchased Covagen AG in 2014 primarily for their lead product, COVA 322, a bispecific anti-tumor necrosis factor in Phase 1b clinical trials for psoriasis with the potential to treat a broad range of inflammatory diseases (9). The historical probability of technical and regulatory success for investigational compounds in the Autoimmune/Inflammation therapeutic area from Phase 1 to Approval is 15.1% (10), but Johnson and Johnson utilized a higher 26% probability of success factor when determining the present value of COVA 322 (11). This adjustment was likely made to reflect the fact that tumor necrosis factor is a validated target in this disease and the higher historical probabilities of success with antibody-based products.

The discount rates and probability of success factors Johnson and Johnson used when calculating the value of other products in the midst of research and development are outlined in Table 4.

Theoretical Example

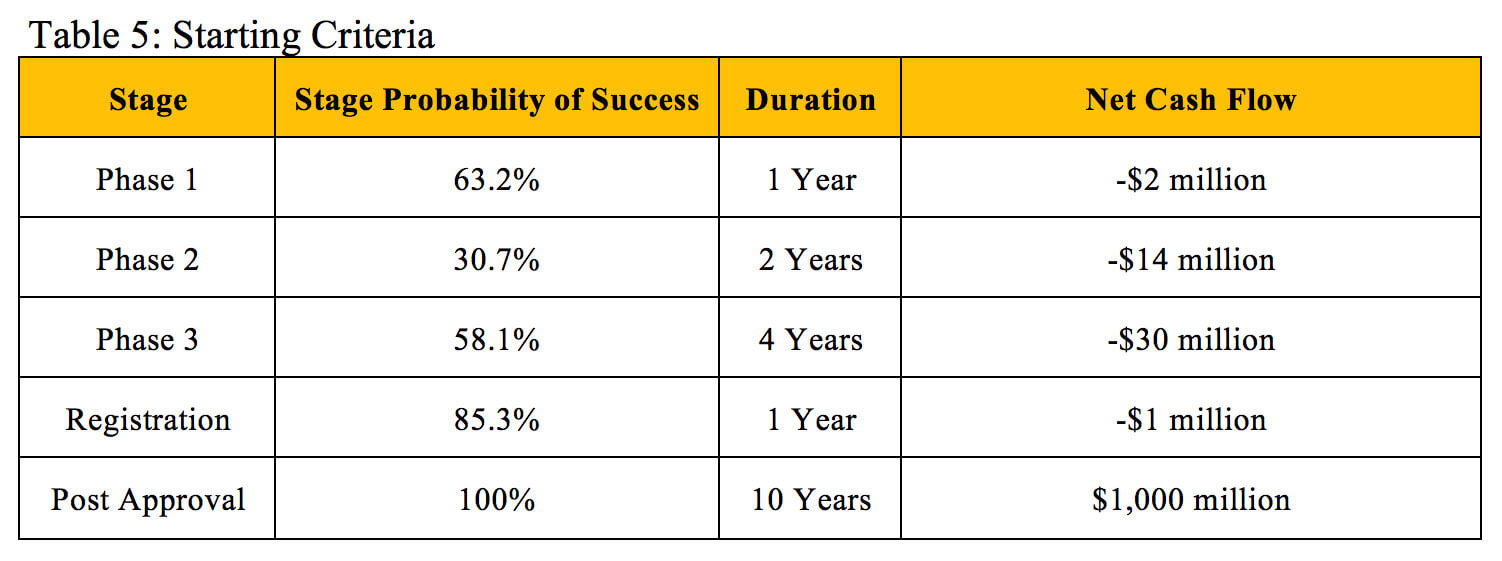

To illustrate how NPV and rNPV calculations can result in similar valuations, we will use a hypothetical investigational new drug with the criteria outlined in Table 5 that is about to enter Phase 1 clinical trials. The cost, duration and probability of success of each stage fall within the average ranges experienced across therapeutic areas (12). The drug is estimated to generate a flat $100 million in profit during each of the 10 years it remains on the market before its patent expires.

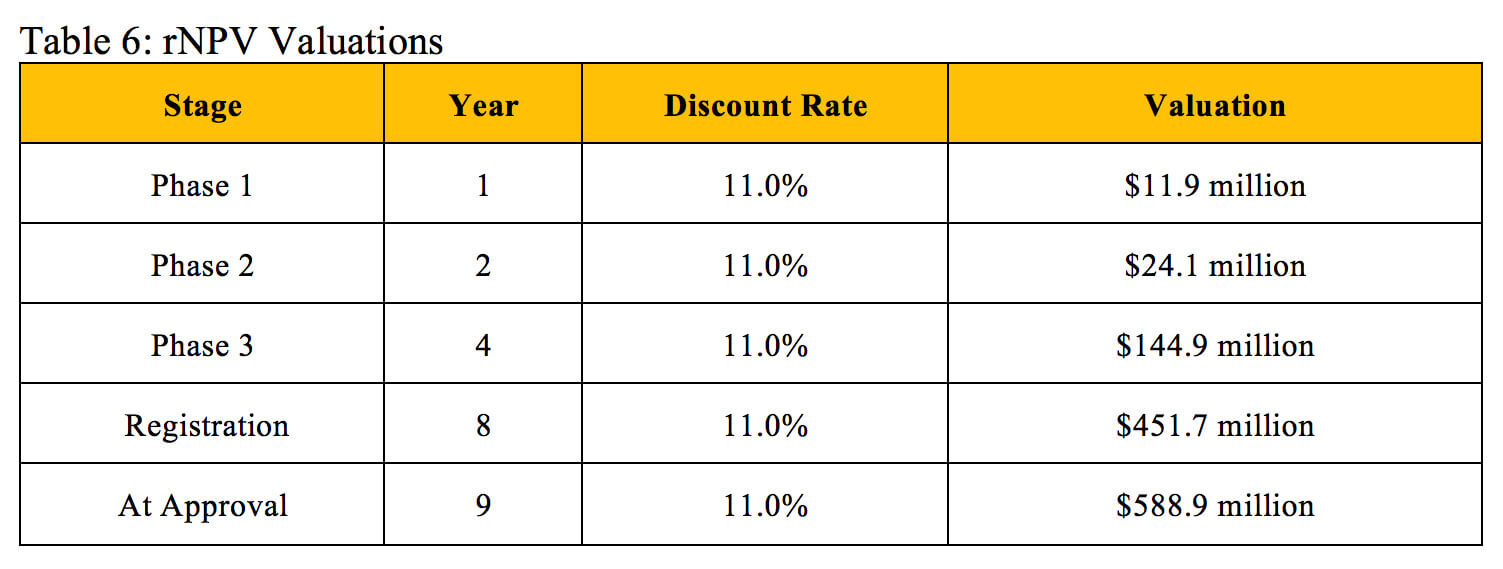

The valuations in Table 6 result from performing rNPV calculations at each stage based on the established criteria using an 11% discount rate.

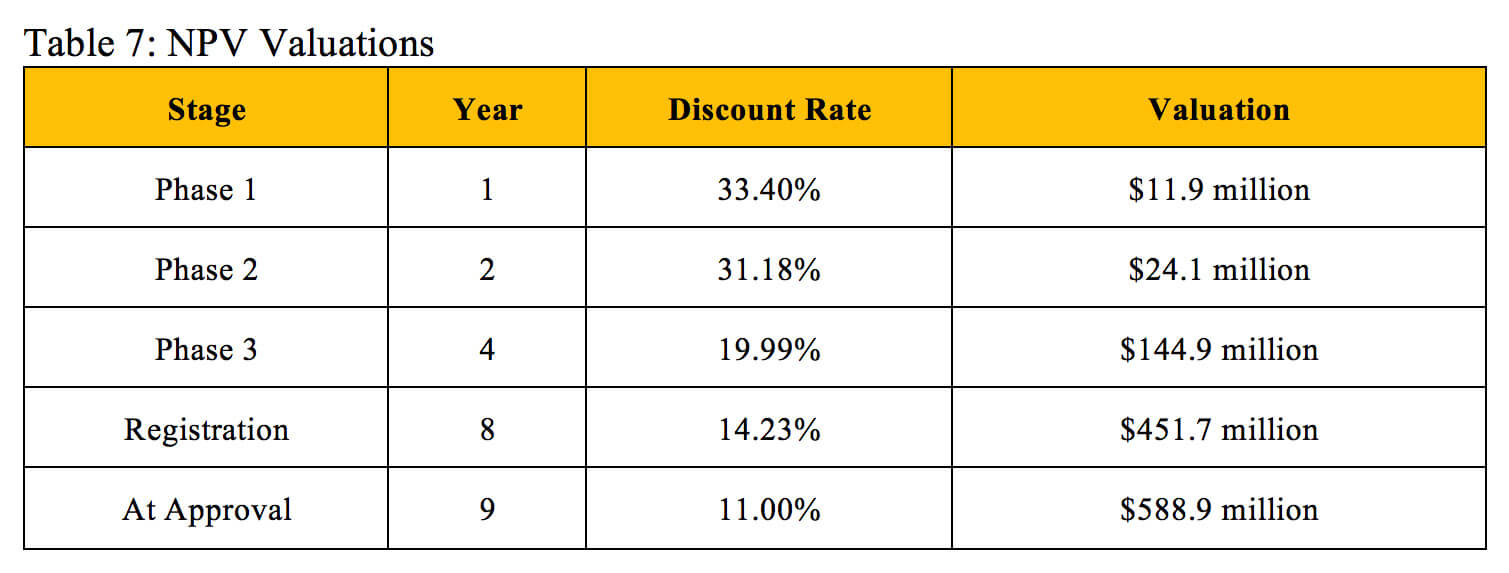

Table 7 displays valuations found through the NPV method and derives corresponding discount rates that align with the identical valuations at the same stages of development found using the rNPV method.

Our derived NPV discount rates generally match the industry benchmarks listed in Table 2. Biotech professionals use an average discount rate of 40.1% to calculate the NPV of early-stage projects, which also include pre-clinical assets, so this rate should slightly exceed our derived Phase 1 discount rate. The industry benchmark of 26.7% for mid-stage projects falls extremely close to the average of our derived Phase 1 discount rate and Phase 2 discount rate. The 19.5% benchmark for late-stage projects falls between our derived Phase 3 discount rate and Registration discount rate. While the industry standards for NPV discount rates do not perfectly reflect the overall probability of technical and regulatory success used in the rNPV calculation, they can provide a similar and reasonably accurate valuation at an individual stage of development.

NPV vs rNPV

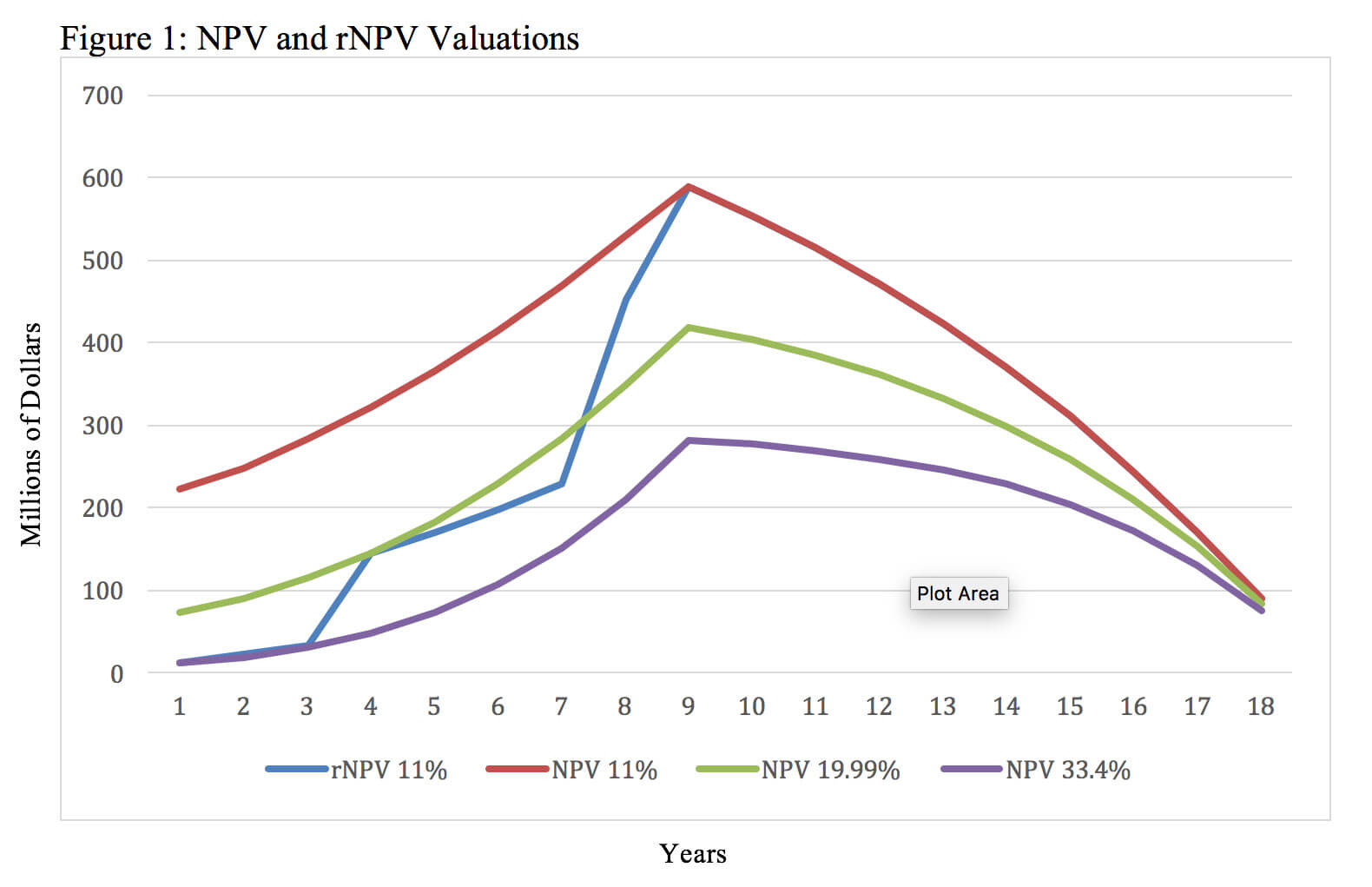

If both the NPV and rNPV approaches can yield similar valuations, then why would a stakeholder choose to use rNPV when it requires supplemental information and more complicated math? Although the two methods can yield the same valuation at a given point in time, rNPV calculations better reflect changes in the investigational new drug’s present value over time while it advances through clinical trials. This cannot be accomplished using the NPV method because the calculation does not have a mechanism other than the discount rate to account for research and development risk. Figure 1 uses the same assumptions outlined in Table 6 and illustrates four different valuations at each year before the patent expires. These values were generated using an rNPV calculation with an 11% discount rate, an NPV calculation with a 33.4% discount rate, an NPV calculation with a 19.99% discount rate and an NPV calculation with an 11% discount rate.

Figure 1 illustrates that while both methods can result in the same valuation at a particular point in time, the rNPV approach provides insights about the investigational new drug’s value at multiple points in time. The NPV approach requires the use of different discount rates in an attempt to approximate the evolving probability of technical and regulatory success. Each new NPV calculation and discount rate can only provide insight about the net present value and risk at a single point in time. For example, the NPV calculation with a 33.4% discount rate yields the same valuation as the rNPV method during year one, but an NPV calculation with a discount rate that high overestimates the risk during the later phases of development and post approval. This results in greatly undervaluing the asset through most of its lifecycle. Similarly, the NPV calculation with an 11% discount rate yields the same valuation as the rNPV calculation after launch, but it underestimates the risk during the earlier phases of development. This contrasts with rNPV derived valuations that increase over time as the product advances through clinical trials with the corresponding value inflection points after successful completion of Phase 1, Phase 2 and Phase 3 clinical trials.

The rNPV method allows for analyzing an in-process research and development asset’s (potential) value throughout all stages of development. This becomes particularly useful when one needs to evaluate key strategic decisions like when to raise capital and when to out-license or partner an asset. Additionally, this proves helpful when negotiating in or out licensing of an asset and quantifying the appropriate value of developmental milestone payments becomes necessary.

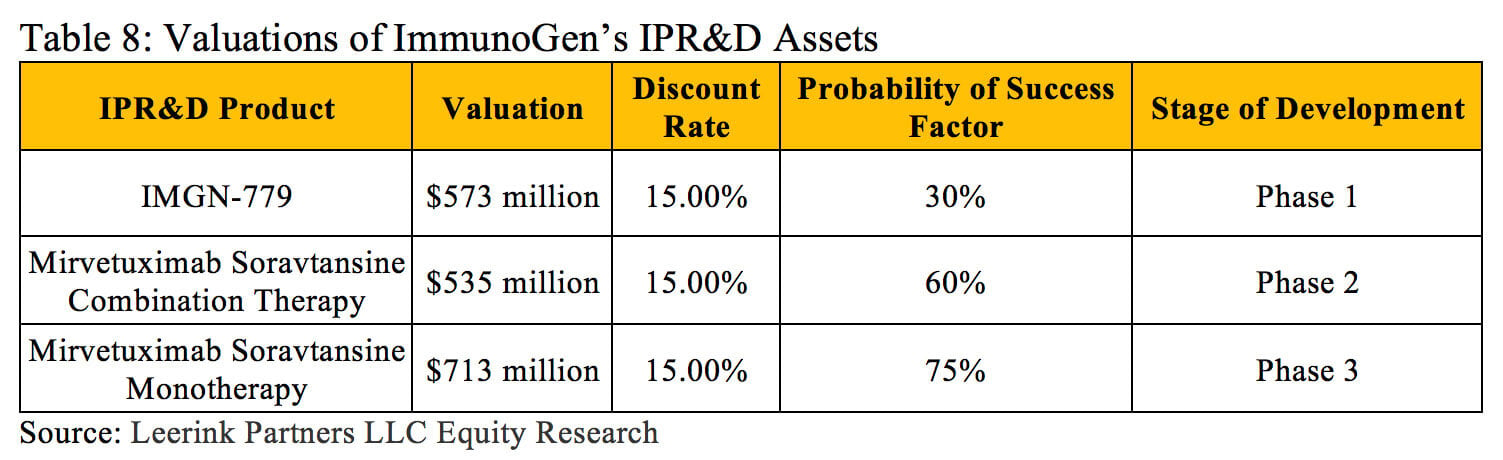

The rNPV approach also provides advantages when a company has multiple drugs in development within different therapeutic areas. Each new drug may have its own probability of success at each stage of development depending on its therapeutic class, mechanism of action, molecular size, etc. These specific factors can all be analyzed and accounted for using historical success rate data when determining the value of each asset with an rNPV calculation. For instance, ImmunoGen Inc. currently has three in-process research and development assets, and each has its own characteristics and risk profile (outlined in Table 8) (13).

ImmunoGen’s weighted average cost of capital provides an accurate discount rate for determining the NPV of the entire firm, but using this discount rate to assess the value of each asset would result in widely inaccurate valuations. The rNPV method can further support the portfolio planning process when companies attempt to prioritize multiple R&D projects under consideration.

In summary, the NPV method simply and easily determines the current value of an in-process research and development asset based on its expected revenues/costs and the overall risk of it failing to reach the market. When investors want to determine the value of a drug development company or the collective value of all its assets, the company’s weighted average cost of capital provides a reasonable discount rate for calculating NPV. The NPV approach can provide enough information to adequately inform purchase/investment decisions that primarily rely on the current value of the asset. The rNPV method constitutes a more involved and complicated approach, but relying on clinical trial success rate data to incorporate risk into the calculation often results in a more accurate valuation. It also can reflect the decreasing risk of an asset at multiple stages of development without having to perform new calculations with different discount rates. This approach allows stakeholders to make decisions that capture future value as it is created while reflecting the nuances around the variance of probability at each individual stage of development. These characteristics make the rNPV method an extremely useful and dynamic tool. A wide range of stakeholders employ both methods, so understanding the underlying calculations, their differences and the factors that play the largest role in determining the resulting valuations remains important.

References

1. Thomas, D. W., Burns, J., Audette, J., Carroll, A., Dow-Hygelund, C., & Hay, M. (2016, June). Clinical Development Success Rates 2006-2015.

2. NPV vs. RNPV. Avance. February 2011. www.avance.ch/newsletter/docs/avance_ on_NPV_vs_rNPV.pdf. Accessed June 20, 2018

3. Bogdan, B. & Villiger, R., Valuation in Life Sciences 3rd Ed., doi 10.1007/978-3-642-10820-4_2, Springer-Verlag Berlin Heidelberg (2010)

4. Festel, G., Wuermseher, M. Cattaneo, G. (2013), Valuation of Early Stage High-tech Start-up Companies, International Journal of Business, 18, 216-231.

5. Baras AI, Baras AS, Schulman KA. Drug development risk and the cost of capital. Nat Rev Drug Disc. 2012; 11: 347-348. PMID: 22498751.

6. Bratic, V.W., Tilton, P., and M. Balakrishnan, 2000. Navigating through a biotech valuation. Working paper, PricewaterhouseCoopers LLC.

7. Villiger R, Nielsen NH. Discount rates in drug development. January 2011. http://www.avance.ch/avance_biostrat_discount_survey.pdf. Accessed June 20, 2018

8. Stewart, J.J., Allison, P.N., & Johnson, R.S. (2001). Putting a price on biotechnology. Nature Biotechnology, 19(9), 813-818.

9. Johnson & Johnson Services, Inc. (2014, August 25). Janssen Affiliate Cilag GmbH International Acquires Covagen AG. Retrieved June 26, 2018, from https://www.jnj.com/media-center/press-releases/janssen-affiliate-cilag-gmbh-international-acquires-covagen-ag

10. Chi Heem Wong, Kien Wei Siah, Andrew W Lo; Estimation of clinical trial success rates and related parameters, Biostatistics, kxx069, https://doi.org/10.1093/biostatistics/kxx069

11. Johnson & Johnson. (2018, March). The Johnson and Johnson 2016 Annual Report. Retrieved June 26, 2018, from https://jnj.brightspotcdn.com/88/3f/b666368546bcab9fd520594a6016/2017-0310-ar-bookmarked.pdf

12. Sertkaya, A., Wong, H., Jessup, A., & Beleche, T. (2016). Key cost drivers of pharmaceutical clinical trials in the United States. Clinical Trials, 13(2), 117-126. doi:10.1177/1740774515625964

13. Leerink Partners LLC Equity Research. (2018, May 15). Immunogen, Inc. KOLs Discuss Mirvetuximab Ahead of Multiple Data Readouts over Next 12 Months. Retrieved June 26, 2018.